Weak employment is eroding popular support for the policy mix, clouding Argentina’s outlook beyond the 2027 vote. Modest policy adjustments, we argue, could go a long way to reassure voters and investors.

The June upgrade of Argentina’s sovereign rating by S&P Global reflected progress with the country’s macro rebalancing required to return to a sustainable growth path1. For markets, the result of Argentina’s improved fundamental picture is a narrower range of potential outcomes. And that marks a break from a past of recurrent bouts of economic and financial instability. The economy has been on a steady, if uneven, recovery since mid-2024 led by primary sectors (labor-intensive areas like retail and construction remain sluggish). The commitment to fiscal discipline is addressing a historical vulnerability, namely Argentina’s habit of living beyond its means, while also contributing to the disinflationary process2. Multilateral funding is buying time for authorities to keep rebuilding external buffers3. Regaining full market access - the final test of debt sustainability - would probably require more active management of the yield curve through exchanges before the door opens to new debt issuance.

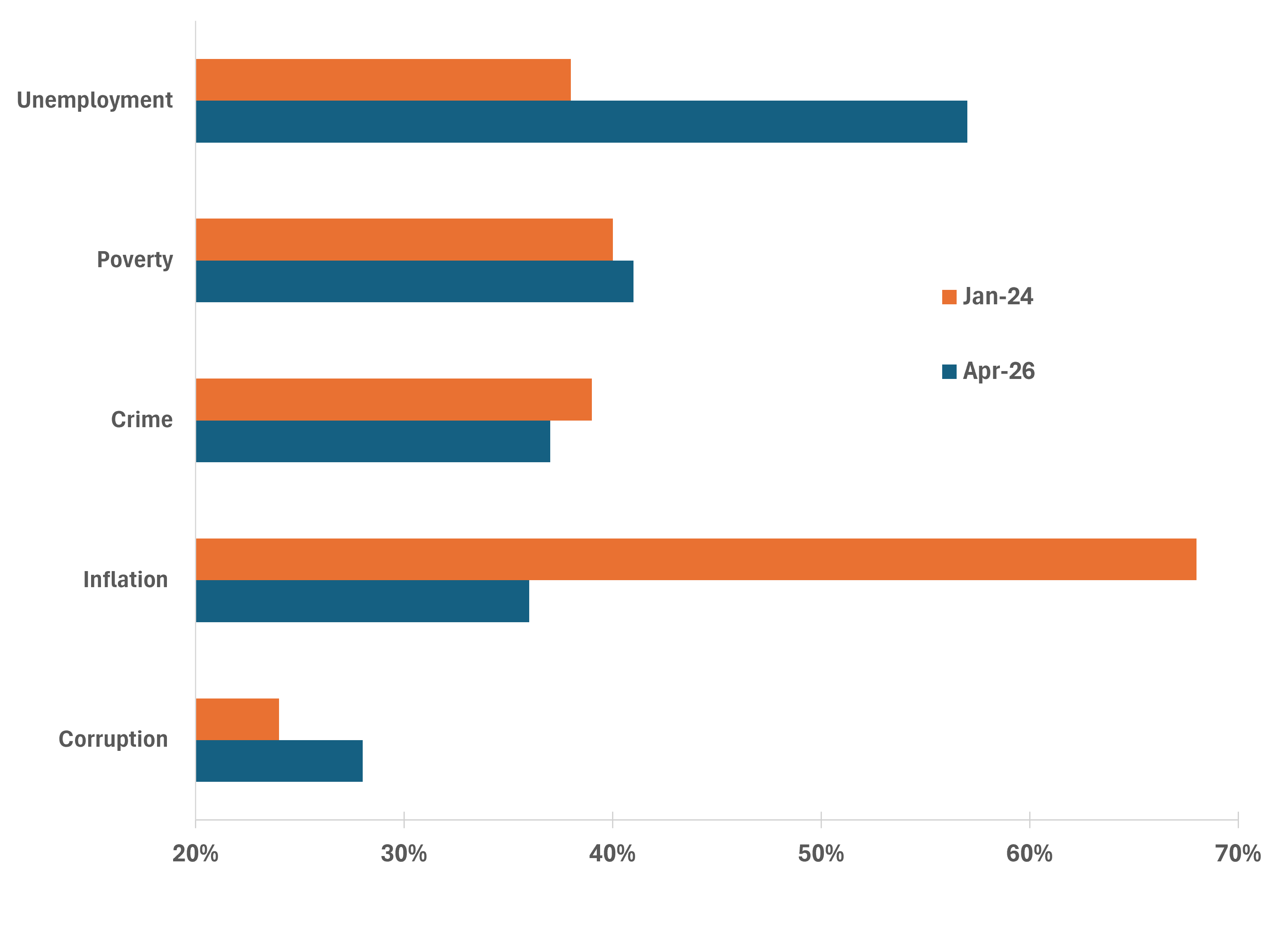

An alignment between the administration, market participants and the population has been instrumental to the success of the rebalancing. Early on, the population tolerated the economic pain – as evidenced by the resilience in President Milei’s approval throughout 2024 – from policies necessary to bring triple-digit inflation under control. In fact, around the time when President Milei took office, inflation was Argentines’ top concern with 68% of participants in a survey calling it as one of their top three worries4 (see Figure 1). Yet that alignment is now under pressure and the source of the tension seems to be mounting concerns over sluggish job growth, which is leading to reform fatigue5. Today, unemployment (57%) and poverty (41%) replaced inflation as consumers’ top worries4.

Figure 1: Jobs and poverty top concerns among Argentines (% of answers, question: what are your top three concerns?)

For investors, the critical question is if the current policy mix can ensure continued popular support for the pro-business agenda – the anchor of Argentina’s investment case. Fiscal discipline, reserve accumulation and deregulation are important steps to rebalance the economy, yet its sustainability hinges on its ability to boost investment and jobs. Market fears about an electoral setback, we suspect, come mainly from voters’ perception that the economy isn’t delivering for them5. And mounting investment pledges in primary sectors are unlikely to generate benefits — tax receipts, inflows, jobs — soon enough6. Bolstering popular support until then, we think, does not require major policy reversals, just adjustments on three key fronts:

Communication – Policymakers keep reassuring investors of the commitment to the fiscal anchor and the capital market strategy, including pledges not to tap external markets. Similarly, they could redouble efforts to communicate with the population how the reform agenda will pay off in terms of jobs and prosperity, while taking steps to alleviate some of the adverse trade-offs. The replacement of the chief of staff, for example, stands as a pragmatic response to popular demands for change7. While Argentina bulls rightly point out that the opposition is weak, the 2027 vote is still far and a lot can shift until then. A fragile opposition also means the government will get the full blame for any shortcomings with the economy or corruption.

Capital controls – Increased investment is necessary to boost growth. Scrapping capital controls on profits generated starting 2025 was a step in the right direction8. However, we think that it is probably not sufficient to reassure investors who either have money trapped in the country — subject to a double standard that penalizes prior investment — or who see remaining controls as a sign that barriers could come back. The recent MSCI decision to keep Argentina out of global stock indices is indicative of the need to further lower barriers to capital9. For policymakers, the trade-off for reassuring investors by providing a path for lowering capital controls is accepting some peso weakness, along with more gradual disinflation.

Investment incentives – The scheme for large-scale projects (RIGI) that provides long-term certainty (tax, regulation, etc.) is attracting interest, mainly in mining and energy10. Yet these commitments involve little actual upfront spending for compliance with the rules, and investors seem inclined to wait for either a weaker currency and/or election results. Moreover, the contradiction of rolling out incentives to new players while limiting the ability of prior investors to repatriate capital adds further uncertainty to capex plans, in our view. After all, investors’ main historical challenge has been dealing with sharp policy reversals and uncertainty. Separately, policymakers unveiled a scheme for capex by smaller companies (RIMI) focusing on tax breaks11. Extending some of the features that make RIGI compelling would help generate investment upfront.

ABOUT TRG

Founded in 2002, The Rohatyn Group (TRG) is a global asset manager focused on emerging markets and real assets. Headquartered in New York the firm is comprised of ~100 professionals based in 14 countries across North and South America, Europe, the Middle East, Africa, India, Southeast Asia, and Oceania.

TRG investment capabilities span private and public asset classes focused on emerging markets as well of global forestry and agriculture investments. At the core of our business, we are dedicated to providing specialized investment solutions. Leveraging our global-meets-local approach, on-the-ground coverage, and extensive multidisciplinary investing experience we work strategically to address our clients’ unique needs.

Learn more at: https://www.rohatyngroup.com/

IMPORTANT INFORMATION – REFERENCES

1 S&P Global. (June 10, 2026). Argentina Long-Term Ratings Raised to ‘B-‘ on Better Access to Financing; Outlook Stable.

2 International Monetary Fund. (May 21, 2026). IMF Executive Board Completes Second Review of the Extended Arrangement Under the Extended Fund Facility and Concludes 2026 Article IV Consultation with Argentina.

3 Buenos Aires Times. (June 4, 2026). Argentina’s dollar buying tops US$10 billion goal on export boom.

4 IPSOS. (January 29, 2024, and April 21, 2026). What Worries the World?.

5 The Economist. (May 5, 2026). Javier Milei is in Serious Trouble.

6 The Net-Zero Circle. (June 18, 2026). Argentina RIGI Pipeline Tops USD 140 Billion — 25 Projects Still Under Evaluation.

7 Reuters. (June 27, 2026). Argentina Cabinet Chief Resigns After Corruption Allegations.

8 Dentons. (April 16, 2025). Removal of foreign exchange controls in Argentina.

9 Bloomberg. (June 23, 2026). MSCI Upgrades Bulgaria to Frontier; Vietnam, Argentina Unchanged.

10 EIU. (July 25, 2024). Argentina’s new investment promotion regime: key points.

11 Dentons. (March 6, 2026). Argentina Introduces the Incentive Regime for Medium-Sized Investments (RIMI)

IMPORTANT INFORMATION – DISCLAIMERS

The information provided herein is for educational and informational purposes only, and neither The Rohatyn Group nor any of its affiliates (together, “TRG”) is offering any product or service hereby. The information provided herein is not a recommendation, offer, or solicitation of an offer to buy or sell any security, commodity, or derivative, nor is it a recommendation to adopt any investment strategy or otherwise to be construed as investment advice. Any projections, market outlooks, investment outlooks or estimates included herein are forward-looking statements, are based upon certain assumptions, and should not be construed as an indication that certain circumstances or events will actually occur. Other circumstances or events that were not anticipated or considered may occur and may lead to materially different outcomes. The information provided herein should not be used as the basis for making any investment decision.

Unless otherwise noted, the views expressed in the content herein reflect those of the authors set forth and are not necessarily the views of TRG. In fact, the views of TRG (and other asset managers) may diverge significantly from certain of the views expressed in the content herein. The views expressed in the content herein are subject to change without notice, and TRG disclaims any responsibility to furnish updated information in the event of any such change in views. Certain information contained herein has been obtained from third-party sources. While TRG deems such sources to be reliable, TRG cannot and does not warrant the information to be accurate, complete or timely, and TRG disclaims any responsibility for any loss or damage arising from reliance upon such third-party information or any other content provided herein.

Exposure to emerging markets generally entails greater risks and higher volatility than exposure to well-developed markets, including significant legal, economic and political risks. The prices of emerging market exchange rates, securities and other assets are often highly volatile and movements in such prices are influenced by, among other things, interest rates, changing market supply and demand, external market forces (particularly in relation to major trading partners), trade, fiscal and monetary programs, policies of governments and international political and economic events and policies. All investments entail risks, including possible loss of principal. Past performance is not necessarily indicative of future performance.

The information provided herein is neither tax nor legal advice. You must consult with your own tax and legal advisors regarding your particular circumstance.